Fix and Flip Loan Overview: Greenwich, CT

A husband-and-wife investment team based in Fairfield County purchased a distressed single-family home in Greenwich’s Byram neighborhood for $280,000 cash. The renovation they had planned carried a $400,000 price tag, representing 143% of the property’s as-is value at the time of acquisition.

Stormfield underwrote the transaction based on the strength of the sponsorship, the quality of the asset coverage, and direct knowledge of the Greenwich submarket. The deal required a program exception on the rehab-to-as-is-value cap. The exception was approved. Stormfield closed a $475,000 fix and flip loan through its fix and flip loans Connecticut program in April 2025. When the property was sold in February 2026 at $1,215,000, it came in $149,250 above the underwritten ARV of $1,065,750. Gross profit to the borrowers: $495,000 at a 68.75% margin.

Deal Snapshot

| Location | Greenwich, CT (Byram neighborhood, Fairfield County) |

| Asset Type | Single-Family Residential, Fix & Flip Loans, Connecticut |

| Investor Profile | Experienced repeat borrower; Fairfield County residents; owner-operators of a full-service GC firm |

| Purchase Price | $280,000 (cash acquisition, June 2024) |

| Renovation Budget | $400,000 |

| Underwritten ARV | $1,065,750 |

| Loan Amount | $475,000 |

| Closing Date | April 23, 2025 |

| Total Project Duration | Approximately 10 months (April 2025 to February 2026) |

| Exit Price | $1,215,000 (February 2026) |

| Gross Profit | $495,000 at a 68.75% gross margin |

| Timeline vs. Plan | Closed on schedule; renovation and sale completed within 12-month loan term |

The Fix & Flip Loan Opportunity

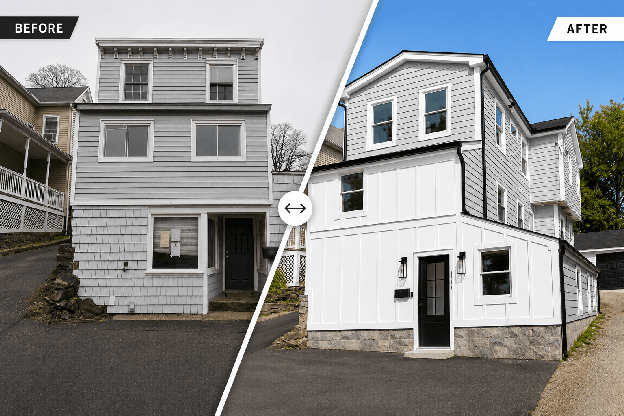

The sponsors identified a distressed 136-year-old single-family home in Greenwich’s Byram neighborhood as a value-add opportunity. At acquisition, the home was a 2-bedroom, 1-bathroom property in poor condition. Byram sits at a lower price point than much of Greenwich but carries the same address, commuter access, and long-term demand, characteristics that make it well-suited to value-add strategies, including fix and flip loans in Connecticut.

The sponsors planned a full gut renovation with a modest addition, converting the home into a 3-bedroom, 4-bathroom property at 1,332 sq. ft. Before approaching Stormfield for financing, the sponsors had already pulled permits and finalized plans in the months following their June 2024 cash purchase.

One factor that sets this deal apart: the sponsors own the general contracting firm that executed the work, eliminating third-party contractor dependency and keeping both budget and timeline under direct control.

Challenges in Fix and Flip Loans Connecticut

The transaction presented several structural challenges that made conventional financing difficult to obtain.

Rehab-to-As-Is-Value Ratio

The renovation budget represented approximately 143% of the property’s as-is value, well outside the parameters of many conventional fix-and-flip lending programs.

The stacked exception structure likely would have required material restructuring under many standardized bridge lending programs.

Additional Underwriting Challenges for Fix and Flip loans in Connecticut

Institutional lenders operating under fixed program guidelines would likely have encountered several additional barriers to the transaction:

- Asset age and condition: the property was built in 1889 and rated in poor condition at underwriting, with significant deferred maintenance

- Lot constraints: the 0.08-acre lot added complexity in a market where larger residential parcels are more common

- Submarket familiarity: Lenders without direct knowledge of the Byram neighborhood may have struggled to underwrite the ARV with conviction despite broader Greenwich market demand

- Limited exception flexibility: Many institutional bridge lending programs lack the ability to evaluate layered exceptions outside rigid underwriting matrices

The combination of these factors meant the transaction likely would have been declined or materially restructured by many institutional lenders before underwriting could fully evaluate the sponsorship strength or collateral coverage.

A lender that could not accommodate the rehab-to-AIV exception would have left the borrowers with one option: cut the renovation scope. That would have compromised the value-add thesis and reduced the return the deal was capable of generating.

Asset Age and Condition

The property was built in 1889 and rated in poor condition at underwriting, with significant deferred maintenance and a constrained lot of 0.08 acres. Standard credit matrices treat vintage assets in poor condition as elevated risk, often without the ability to account for compensating factors.

Without a lender willing to approve the rehab-to-AIV exception, the borrowers would have been unable to execute the full renovation scope. A reduced renovation would have diluted the value-add thesis and the return potential of the deal.

How Stormfield Underwrites Fix and Flip Loans in Connecticut

Stormfield evaluated the transaction on the basis of sponsorship quality, collateral coverage, and direct submarket knowledge.

Sponsorship

The borrowers are Fairfield County residents with demonstrated knowledge of the Greenwich submarket. They own the general contracting firm executing the renovation, which removed third-party contractor dependency as an execution risk. The guarantors had strong FICO scores, sufficient liquidity, and verified experience managing active investment properties.

Collateral Coverage

The property’s condition at underwriting was poor, but the loan structure produced leverage ratios that kept the collateral position conservative throughout:

- Day-One Loan-to-as-is value (LTAIV): 26.79%

- Loan-to-after-repair value (LTARV): 44.57%

- Property was free and clear at underwriting with no existing liens

The asset coverage gave Stormfield confidence that the collateral position was sound even under a stress scenario.

Submarket Knowledge

Stormfield has direct familiarity with the Byram neighborhood of Greenwich. That knowledge informed the underwritten ARV of $1,065,750 and provided confidence in the exit strategy. The deal was not being modeled from a distance.

The program exception on the rehab-to-AIV cap was approved based on the combination of these factors. The stacked complexity of the deal, the asset age, condition rating, and rehab ratio, was offset by the strength of the sponsorship, the low LTV ratios, and Stormfield’s conviction in the submarket and exit.

Structuring the Fix and Flip Loan Solution

The fix and flip loan Stormfield structured addressed two needs: immediate day-one funding and a full renovation reserve, released in stages tied to construction milestones.

| Total Loan Amount | $475,000 |

| Day-One Funding | $75,000 |

| Rehab Reserve | $400,000 (disbursed in 3 milestone-based draws) |

| Interest Reserve | $15,000 (prepaid via day-one funding) |

| Loan Term | 12 months |

| Rate | 9.99% fixed, interest-only |

| Origination Fee | 1.00% |

| Exit Fee | 1.00% |

| LTC | 65.97% |

| LTARV | 44.57% |

| Day-One LTAIV | 26.79% |

| Program Exception | Rehab-to-AIV cap waived (143% vs. 100% standard program maximum) |

Fix and Flip Lending Timeline

| Milestone | Planned | Actual |

|---|---|---|

| Initial Inquiry | Early April 2025 | Early April 2025 |

| Term Sheet Issued | Early April 2025 | Early April 2025 |

| Underwriting Complete | Mid-April 2025 | April 16, 2025 |

| Closing | Late April 2025 | April 23, 2025 |

| Draw 1 | Post-close | Post-close |

| Draw 2 | Mid-renovation | Mid-renovation |

| Draw 3 (Final) | Months 5 to 6 | September 2025 |

| Renovation Complete | Within the loan term | On schedule |

| Exit / Sale | Within 12 months | February 2026 |

Execution in Practice

At Closing

What was agreed at the term sheet is what closed. No pricing changes, no structural adjustments. The draw schedule and disbursement process were laid out before work started, so the borrowers knew exactly what to expect at each stage of the renovation.

During Renovation

The $400,000 rehab reserve was disbursed across three milestone-based draws. The final draw was completed in September 2025. Because underwriting and loan servicing are managed by the same team at Stormfield, the draw process was consistent with what was agreed at closing. There were no delays caused by third-party inspection dependencies or internal misalignment.

The borrowers maintained direct communication with the Stormfield team throughout the renovation period. The renovation was completed within the 12-month loan term, on schedule and on budget, a result supported in part by the borrowers’ ownership of the GC firm.

Outcome

Financial Outcome

- Exit price: $1,215,000 (February 2026)

- Underwritten ARV: $1,065,750

- Exit price exceeded underwritten ARV by $149,250 (approximately 14%)

- Gross profit: $495,000 at a 68.75% gross margin

- Project completed within the 12-month loan term, on schedule

Execution Outcome

- $400,000 rehab reserve disbursed across 3 draws with no funding delays

- Renovation completed on budget through sponsor-managed general contracting

- No draw delays caused by third-party inspection or servicing dependencies

- Borrowers maintained the contractor schedule throughout the renovation period

The financing structure allowed the borrowers to execute the full renovation scope without interruption, avoid cost overruns that typically follow funding delays, and preserve liquidity for concurrent projects rather than self-funding a $400,000 renovation.

Borrower Perspective

Why They Chose Stormfield

The borrowers were referred to Stormfield through a broker partner. A key factor in their decision was Stormfield’s familiarity with the Greenwich submarket, which gave them confidence that the lender understood the asset, the exit, and the exception they were asking for.

What Mattered Most

Certainty of execution. Given the exception-heavy structure of the deal, the borrowers needed confidence that the terms agreed at the term sheet would hold through closing, and that the draw process would run as expected through the renovation. Prior experience with lenders who created friction at the draw stage made that consistency a priority.

Why This Fix & Flip Loan Matters for Connecticut Investors

This transaction illustrates what flexible, balance sheet-backed underwriting looks like when applied to a deal that falls outside standard parameters. The rehab-to-AIV ratio was a genuine exception, not a technicality. It required a deliberate credit decision based on a clear view of the sponsorship, the collateral coverage, and the submarket.

The result, a $1,215,000 exit, $149,250 above the underwritten ARV, and $495,000 in gross profit, reflects both the borrowers’ execution and the underwriting conviction that made the deal possible.

For borrowers pursuing value-add acquisitions that require structural flexibility, the ability to access a lender with direct balance sheet authority and genuine submarket knowledge is often the variable that determines whether a deal gets done.

Why Stormfield For Fix & Flip Loans

Stormfield is structured for transactions that require more than a standard program. Direct balance-sheet capital and in-house credit authority allow Stormfield to evaluate exceptions on their merits without committee delays or rigid program caps that cannot accommodate deal-specific context.

- Flexible structuring: Stormfield can approve program exceptions where the credit case supports them, drawing on direct capital and in-house underwriting authority

- Direct balance sheet lending: Stormfield deploys its own capital, which enables faster decisions and greater structuring flexibility than lenders dependent on third-party funding

- Hyperlocal underwriting: direct knowledge of submarkets like Byram in Greenwich informs ARV confidence and deal-level conviction that generalist lenders cannot replicate

- Certainty of execution: terms agreed at issuance are honored at closing; draws are processed without third-party dependency; borrowers can execute their business plan without managing financing risk alongside it

Borrowers working on complex value-add acquisitions need a lender who can evaluate the full picture. Stormfield is built to do that.

This is one of many transactions we’ve closed across the state; explore other fix and flip deals funded by Stormfield in Connecticut.

Ready to move? Stormfield delivers Connecticut fix and flip loans built for speed and certainty.