In the 2026 Massachusetts real estate market, cash is your enemy. If you are using leverage, you are not just competing on price; you are competing on speed.

ATTOM reports that over 60% of flipped homes were bought with cash.

The cash trend makes it harder for leveraged investors like you, who are using fix and flip financing to compete, unless you can show you have the cash to close.

Sellers want certainty. A pre-qualification letter does exactly that. It serves as proof of funds (POF). It gives sellers confidence that your financed offer can close as quickly and reliably as cash.

Stormfield Capital has developed a Pre-Qualification tool that turns your project numbers into a pre-qualification letter.

Why Massachusetts Investors Need a Fix and Flip Pre-Qualification Tool

Imagine you have identified a property to flip in Worcester just before a long weekend. You need a pre-qualification letter to compete with cash buyers.

With the Worcester metro area among the top three hottest housing markets in the United States, waiting for a loan officer to be available after a long weekend is a dead end.

In a market where cash buyers move instantly, proving your own financial muscle 24/7 is the only way to stay in the game.

For investors using a fix and flip loan, a self-service Pre-Qualification tool acts as a “POF Plus.” The tool lets you play out scenarios and generate a pre-qualification letter based on the numbers of your specific deal: Purchase Price, Rehab Budget, and ARV.

Your letter proves to a seller that you are not just “looking” for a loan, but have an immediate, green light to move.

Want to know more about the market outlook and investment strategies in MA for 2026? Refer to the blog: Fix & Flip Loans in MA: 2026 Market Outlook & Investment Strategies

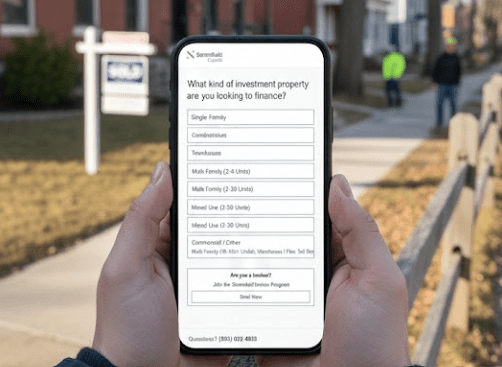

Build Your MA Fix and Flip Pre-Qualification Letter in Under 5 Minutes

Tap through a few screens of Stormfield Capital’s pre-qualification tool. Answer the simple questions, and get to the “Estimate Your Rates and Options” screen.

Input your purchase price, your estimated rehab cost (use real Massachusetts costs), and the ARV. The tool generates the fix-and-flip loan range for which you qualify. You key in the loan amount.

Instant Result: The tool generates your Estimated Rate, Points, and Loan Details. Download your Pre-Qual Letter and Loan details. A letter that proves to any listing agent or seller that you mean business.

MA Rehab Loan Estimator Accuracy: Costs That Impact Your Flip Profit

The fix and flip tool handles the loan logic, but the tool is only as sharp as your numbers.

In Massachusetts, the 2026 labor and materials costs remain high. A shortage of skilled trades in the Northeast means your budget can vanish if you guess wrong.

The Profit Killers: Don’t use a flat square-foot calculation. A 200-sq.-ft. kitchen renovation carries significantly higher costs per foot than a 200-sq.-ft. bedroom. Similarly, in the Boston and Worcester corridors, the jump from “Rental Grade” to “Luxury Condo” finishes can wreck your budget by $50,000+.

Real Massachusetts Benchmarks:

- Kitchens & Baths: These eat your budget first. In MetroWest, high-end kitchen finishes and full bath guts are the primary drivers of budget creep.

- Worcester & Springfield: While general refreshes might sit at $45 – $80/sq. ft., the age of the housing stock often hides “behind-the-wall” costs (electrical/plumbing). Add a 15% safety net.

- Boston & High-Density Hubs: Strict local codes and logistics push gut renovations well beyond $160/sq. ft.

92.5% LTC: Keep Your Cash for the Next Deal

In a market like Massachusetts, your biggest hurdle isn’t just finding the deal, it’s staying liquid enough to grab the next one while your current project is mid-rehab.

A Simplified Fix and Flip Loan Example:

- Total Project Cost: $700,000

- 80% LTC Loan: $560,000 (Your cash required: $140k)

- 92.5% LTC Loan: $647,500 (Your cash required: $52.5k)

On a typical $700,000 project, the difference is $87,500 back in your pocket. That isn’t just “liquidity”. That is the deposit on your next triple-decker in Worcester or a security blanket for when a “refresh” turns into a full plumbing gut.

By generating the pre-qualification letter, you show a seller you have a 92.5% partner behind you. You are showing them you have the financial backing to close with certainty.

Know Your Costs Before You Sign

Don’t get blindsided at the closing table. Two important questions that you should ask your fix and flip hard money lender:

Q1. How Much Cash Do You Need to Close on a Fix and Flip Loan in MA?

This isn’t just your down payment. It is your down payment plus origination points, legal fees, and prepaid interest.

Q2. What Is the Monthly Carrying Cost of a Massachusetts Hard Money Loan?

A hard money loan is interest-only. As you draw rehab funds, your loan balance and your payment will grow.

Stormfield Capital’s pre-qualification tool not only generates the proof of funds, but also the loan details. You get the answers you need before you even talk to a lender.

Top Fix and Flip Financing Mistakes Massachusetts Investors Must Avoid

1. Ignoring Holding Costs: Interest payments aren’t your only expense. You should factor in property taxes, insurance, and utilities for the full duration of the project.

2. Overestimating the Exit: If you plan to refinance into a long-term rental (BRRRR), evaluate your DSCR (Debt Service Coverage Ratio). If the property doesn’t generate enough cash flow at today’s rates, your exit plan may be at risk.

3. The Appraisal Gap: Most investors assume the appraiser will see the “potential.” In reality, appraisers rely on the most recently sold comps. If there are no $600k sales in the last 6 months, don’t count on a $600k ARV.

After the Pre-Qual Letter: Funding Speed, Draws, and Execution Timeline

A pre-qual letter gets you to the closing table, but the speed of your construction draws determines if you actually hit your profit goals.

There is nothing worse than having a kitchen ready for cabinets but being stuck waiting 10 days for a third-party inspector to clear your funds.

Stormfield has its loan servicing in-house. That means you aren’t dealing with a fragmented “mom-and-pop” setup or a slow institutional middleman. Once you close on your Massachusetts property, your draws are processed with the same urgency as your initial loan. You can keep your momentum, pay your subs on time, and get the property back on the market faster.

Conclusion: Win Massachusetts Fix and Flip Deals With a Pre-Qualification Letter

In the Massachusetts market, the best deals don’t wait for bank approvals or Monday morning callbacks.

If you want to beat cash offers, you need to show up with the same level of certainty.

Use your local knowledge to find the deal and build your budget, then use Stormfield Capital’s pre-qualification tool to lock in your proof-of-funds in minutes. Don’t just “look” at properties; show up ready to close.

Frequently Asked Questions

How do I get pre-approved for a fix and flip loan in MA?

Getting pre-approved is simple. You could visit Stormfield Capital’s instant pre-qualification tool. Key in a few details from the comfort of your mobile and generate the pre-qualification letter.

Do hard money lenders provide proof of funds letters?

Yes, the hard money lenders like Stormfield Capital provide a pre-qualification letter. This letter serves as proof of funds.

What credit score is needed for a rehab loan?

There are many factors that private lenders evaluate. The flip deal is the primary concern, while your credit score is also looked at. Look at the loan page to know more.